One sector in the economy that benefited greatly from the digitization and globalization is the financial sector, that includes especially financial transactions on a national and international scale. While the benefits for said sector are clearly visible, a fair contribution in form of a tax to maintain the infrastructure is missing (a few exceptions being Italy, France and the UK). Regulations, on the other hand, exist for market stability and decrease the volatility. Sustainability, Stability and Safety – to put it in three words.

Introduction

First of all, you may want to know what the financial sector consists of. As defined by Investopedia: It provides financial services to people and corporations. It includes banks, investment houses, lenders, finance companies, real estate brokers and insurance companies. While large conglomerates dominate the sector, it also includes a diverse range of smaller businesses.

As you can imagine, the financial sector therefore makes up a significant part of a country’s economy and the global economy overall. It’s importance is indisputable. With that being said, the stability of this sector is therefore of particular importance (failure example: the Great Recession in the early 2000s).

Moreover, there are three overlapping components the financial services sector has in each country, as elaborated by the ILO (International Labour Organization, affiliated with the UN): „[…] financial enterprises (such as banks) and regulatory authorities; the financial markets (for instance, the bond, equities and currency markets) and their participants (issuers and investors); and the payment system – cash, cheque and electronic means for payments – and its participants (e.g. banks).“

And, a part you may not be aware of yet, the shadow banking system. Quite frankly, it sounds ominous and villainous, that were the exact same thoughts I had. Anyways.

From Investopedia (link above): „Despite the higher level of scrutiny of shadow banking institutions in the wake of the financial crisis, the sector has grown significantly. In May 2017, the Switzerland-based Financial Stability Board released a report detailing the extent of global non-bank financing. Among the findings, the board found that non-bank financial assets had risen to $92 trillion in 2015 from $89 trillion in 2014.“

Furthermore, the ILO elaborates on it as well: „The last decade also saw the spectacular rise of a financial infrastructure, entities and practices collectively referred to as a shadow banking system, comprising among others such businesses as hedge funds, private equity funds, money market funds and special investment vehicles. Many observers believe this shadow banking system, operating outside any national supervisory framework but closely interwoven with the regulated financial system, may have contributed significantly to the onset of the global financial and economic crisis that erupted in the last part of 2008.“

Lastly, while it is difficult to measure the exact size of the global financial services due to inconsistent definitions depending on the data source, no regularly available reports and the World Bank only collecting data from 189 countries while estimating the rest; most put the financial service sector at around 20-25% of the world’s economy.

In numbers: $93,863 billion in 2021 means that the financial sector contributed between $18,772.6 billion to $23,465.75 billion. As already mentioned, it is not precise.

Graph by Statista

Finally, now that we know what the financial sector consists of – while already learning about a more unregulated an unsupervised part of it – we shall continue with the three S – Sustainability, Stability and Safety.

The Three S

Due to the importance of the financial sector and its size, it is only reasonable to pursue continuity through a sustainable system, stability through regulations and safety by implementing a fail-safe system. The latter requires more expertise thought that I cannot provide; an impuls at best by explaining how I’d approach such a fail-safe system.

Sustainability

In this context, sustainability means continuity. Since the financial sector relies on international organisations such as the WTO and UN, it would only be fair if it contributed to it as well. By that, I mean a financial transaction tax. Said tax, even in a conservative scenario, would provide significant revenue. Ideally, on a global level.

I strongly recommend reading the study(PDF)

„A Global Financial Transaction Tax – Theory, Practice and Potential Revenues“ by Atanas Pekanov and Margit Schratzenstaller.

Who bears the burden of a financial transaction tax?

Likely the first question that arises when talking about the FTT.

The burden would be similar to a corporate income tax increase, and following the assumptions of the Tax Policy Center 80% of the burden will fall on capital owners and 20% on labour (Burman et al. 2016, Matheson 2011; p. 17). Furthermore, a microsimulation done by Burman as well shows that, for the US, 75% of the burden would fall on the highest-income quintile while 40% would fall on the Top 1%.

How does the tax affect regular investors?

That’s explained on the same page as well: „[…] most ordinary investors would not be significantly affected by an FTT, as they do not make transactions very frequently, but rather buy assets and instruments to hold them for a longer period based on long-term investment strategies.“ Therefore, the tax would be progressive and spare those who do not engage in high-frequence trading. „Altogether, it can be assumed that an FTT would not have undesirable distributional consequences.“

Has there been an FTT before?

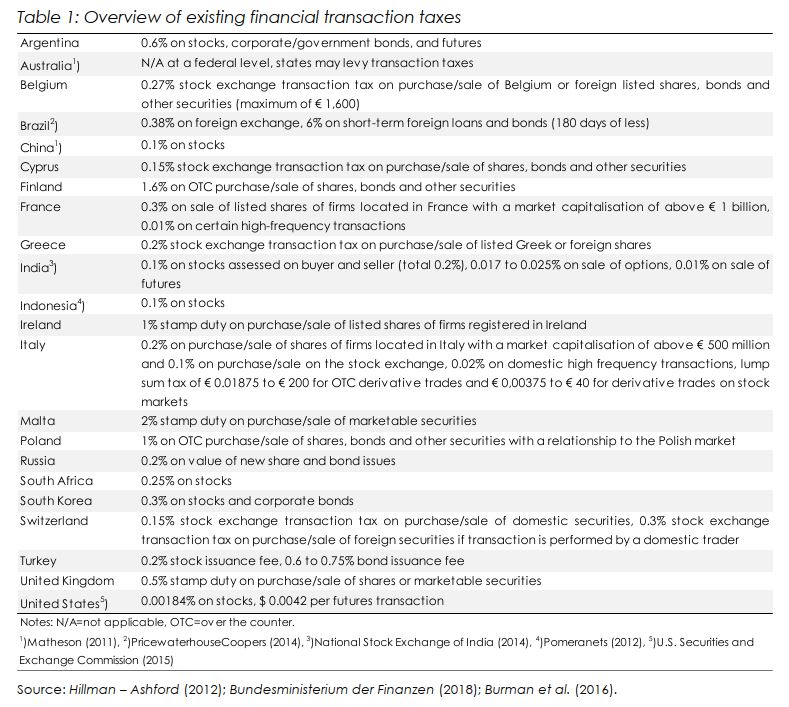

Yes. In the USA, there was a financial transaction tax from 1914 to 1965, during the Great Depression in 1932 it was doubled.

The United Kingdom has a stamp duty tax which has been in place since 1694 and remains to this day. The tax only focuses on stocks and imposes a levy of 0.50%. While it still allows market participants to avoid it, the tax consistently generated £1 to £1.5 billion monthly in the last 5 years.

Japan abolished its FTT in 1999 and 9 Member States of the EU since the end of the 1980s.

In Sweden it was abolished due to its poor design.

Italy and France recently introduced an FTT.

Note: While in Sweden it was abolished due to poor design (see Schulmeister et a. 2008 for more detailed analysis), the motivation in many other countries was to increase competitiveness due to „pressures resulting from the increasing mobility of financial market participants and the decreasings costs of re-locating transactions“ (p. 24).

What would be the potential revenues?

There are three different scenarios that were explored in the study. In case you want to know how it was estimated, you can read it on p. 33 where the formula is as well.

The data sources for Equity Trading was the World Federation Exchange (WFE); for Bonds Trading were used the Federation of European Securities Exchanges (FESE), Securities Industry and Financial Markets Association (SIFMA); OTC Derivative Trading used Bank for International Settlements (BIS) and Triennial Survey; Interest Rate Derivatives and Exchange Traded Derivatives data were from the Bank for Internatioanl Settlements (BIS) as well.

Now to the three estimations.

Conservative Scenario.

Tax rate: 0.1% (trading stocks & bonds instruments), 0.01% (transactions derivatives)

Elasticity: -1.50

Assumption: highest possible evasion and relocation effect (90%) + 15% evasion on bonds and equities (unrealistically high)

Baseline Scenario.

Tax rate: 0.1% (trading stocks & bonds instruments), 0.01% (transactions derivatives)

Elasticity: -1.00

Assumption: 70% evasion and relocation effect + 15% evasion on bonds and equities

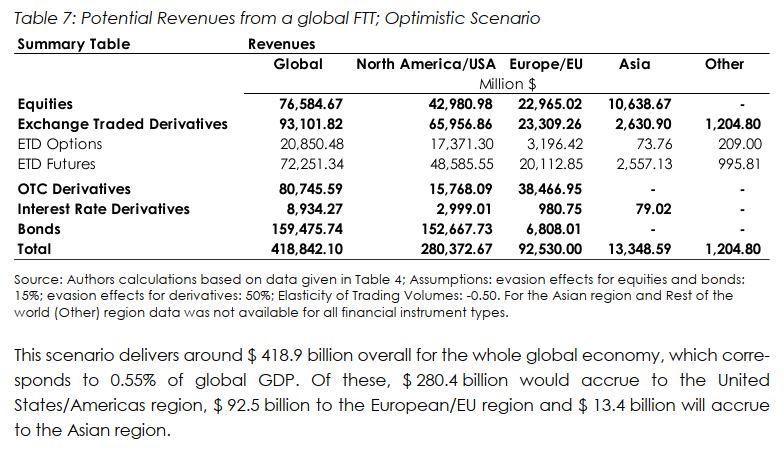

Optimistic Scenario.

Tax rate: 0.1% (trading stocks & bonds instruments), 0.01% (transactions derivatives)

Elasticity: -0.50

Assumption: 50% evasion and relocation effect + 15% evasion on bonds and equities

Moreover, there may be an additional 14% of potential revenues from financial instruments such as Exchange Trade Funds (ETFs), Undertakings for the Collective Investment in Transferable Securities (UCITs), and Alternative Investment Funds (AIFs). However, the authors of the study didn’t have globally comparable data on said instruments.

In the baseline scenario it would be an additional global revenue of $45 billion.

Other reasons why the revenues may be underestimated can be found on page 40 (only half of a page long); a lack of data in the Asian region and some in the rest of the world is mentioned as well.

In case you are interested in a country-by-country revenue, there’s table 8 and table 9 on page 41, respectively page 42.

What about tax evasion?

In order for a financial trans action tax to work with minimal tax evasion, international cooperation is necessary. As the authors said it: „Global and multilateral cooperation will thus be essential for the FTT to be successfully implemented by overcoming fruitless technical discussions and agreeing upon a common design that can raise substantial revenue and ensure it does not disproportionally distort market efficiency.“ (p. 46)

On a national level it can still deliver revenue that is not negligible, as the UK has shown, but there still remain limitations to enforce it due to evasion.

—-

Lastly, this section of sustainability ends with the conclusion of the authors of the study:

„The FTT can raise significant revenues globally. If policymakers and international institutions follow the optimal design of such a tax with a very broad base and a relatively low rate of the tax, the distortionary effects should be quite small. In addition to that, the predominant burden of the tax would be on top wealth groups, which are most active on financial markets. The tax will have a progressive nature, which can also address growing concerns about inequality and distributional fairness. Finally, the FTT enjoys public support and the broad alliance between NGOs and civil society organisation in its favour might make it more feasible to be implemented.

The additional revenues from a global FTT can contribute to the duly needed resources for a number of specific global priorities, where multinational cooperation is essential. In any case, with this amount of potential revenues, an FTT, if designed properly and imposed globally, could help address public calls for the financial sector to contribute more to government budgets and show that international cooperation and multilateral institutions can deliver significant and efficient solutions to the issues of our time.“ (page 47)

Stability

A stable financial sector requires regulations; not only to avoid crises suchs as the Great Depression (1929) and the Great Recession (2007/2008), but to protect the consumers‘ interests, prevent financial fraud and limit the risks a financial institution can take with the money of their investor.

An effective oversight by the government prevents companies from taking excessive risks as well. A real-world example, where tighter regulations would have helped, is Lehmann Brothers. The regulations would have stopped them from engaging in risky behaviour which in turn could have prevented or curbed the 2008 financial crisis.

Regulations and Regulators Examples

- Sherman Anti-Trust Act (prevention of monopolies which abuse their power)

- Federal Deposit Insurance Corporation (FDIC), (examines and supervises more than 5,000 banks)

- Dodd-Frank Wall Street Reform and Consumer Protection Act (strengthened the FED’s power over financial firms)

- The Office of the Comptroller of the Currency (supervisor of all national banks and federal savings associations)

- The National Credit Union Administration (regulates credit unions)

- The Securities and Exchange Commission (SEC), (federal financial regulations, also investigates and prosecutes violations of securities laws and regulations)

- The Consumer Financial Protection Bureau (CFPB), (ensures banks don’t overcharge for credit cards, debits cards and loans)

- 1933 Glass-Steagall Act (regulate banks, after the 1929 stock market crash)

However, this one was overturned 66 years later by the Gramm-Leach-Bliley Act and allowed banks to to invest in unregulated derivatives and hedge funds, and also made it possible for banks to use depositors‘ funds for their own gains;

These are all US examples, but you will find similar/same regulations in other countries.

In recent history, the former President Donald Trump deregulated in 2018:

„The rollback meant the Fed can’t designate these banks as too big to fail. They also aren’t subject to the Fed’s „stress tests. And they no longer have to comply with the Volcker Rule. Now banks with less than $10 billion in assets can, once again, use depositors‘ funds for risky investments.“

The need for regulations won’t change in the future either and, as the Lehmann Brothers example has shown, they can even prevent or curb a crisis. However, it doesn’t stop by simply implementing these regulations. In a democracy, it is also of importance to emphasize the importancy of them and keep the politicians in check as well. A constant back and forth between rollbacks that lead to a crisis, only to re-implement it afterwards by another party, is anything but sustainable and stable. For it both hurts the private sector and the people, especially the working class who has to deal with unemployment and the negative effects that come with it.

Safety

Unlike the other two S’s, the fail-safe is of more theoretical nature. After all, the financial sector is not like a computer file that can simply be restored by making a copy prior once the original has been corrupted.

While we cannot fail-safe the sector in a strict sense, what we do can is preparing politicians for a (looming) crisis. I already explained it thoroughly in my entry called „Political Scenario Simulations for Emerging Politicians (PSSEP)“, here a summary:

- In these simulations, experts are present which evaluate how well the participants responded to it. The participants are allowed to talk to the experts, as they’d naturally do (ideally of course) in the real world.

- There are 3 tests which are conducted, but they are not tested one after another. There’s time in-between (e.g. 2-3 months).

- Various crises can be simulated and, at the end, a certificate is given to the participants.

- The culture of a country also plays a role, if it is implemented in other nations or involves problem-solving with politicians of other nationalities.

Thus, new politicians can gather experience and are better prepared for a crisis. They also learn how to prevent one in the first place.

Even if we implement all regulations that are necessary, as well as the global financial transaction tax, there will still be other threats that can lead to destabilization to some part and which must be prepared for (perhaps most of them already have been prepared for):

- Nature catastrophes and weather extremes due to climate change

- Terrorism

- War

- Humanitarian crisis

Unless there’s been an error in the „file“ before it got corrupted, the goal will be to restore the financial sector (and with it the economy) to its condition before the crisis.

Perhaps, there can even be policies designed that serve as a emergency cord. Thus allowing for a quick response depending on the kind of crisis that a country faces.

Basically, imagine it like an emergency provision: it may not taste well, but it ensures your survival until you get better food.

(The analogy is very likely not ideal, but you get the idea)

End

That’s it from my part, and as always: constructive criticism and polite discussions are welcome! Have a nice day!